The US President recently signed into law a USD 1.2 trillion infrastructure spending plan to provide much needed acceleration to post-COVID economic recovery. As much as this investment plan is promising for US’ slacking productivity and employment growth, it also promises significant growth for global trade flows and overall global economy. An overview.

Recently passed US infrastructure plan aims to put additional funds into financing physical infrastructure including surface transportation, rail transit, highway safety, motor carrier safety, drinking water and sanitation infrastructure, broadband internet, power infrastructure and climate change technology. The USD 1.2 trillion infrastructure bill passed in the US Senate last week includes USD 550 billion of new spending over the next 10 years along with the usual spending on physical infrastructure. Such a large infrastructure spending plan comes a long time after the infrastructure boost in the US post World War II. Notwithstanding, that the US infrastructure needs have remained unmet and this budget could help bridge a small part of that gap, this spending plan is expected to help the US economy recover much stronger from the pandemic induced shock. The plan is also aimed at enabling job creation in the economy, providing a significant growth in productivity levels in the US and build its infrastructure in comparison with China’s Belt and Road investment. However, important it may be strategically for US, this plan is extremely crucial for a much-needed global growth and global trade revival.

Slow US economic growth and need for infrastructure push

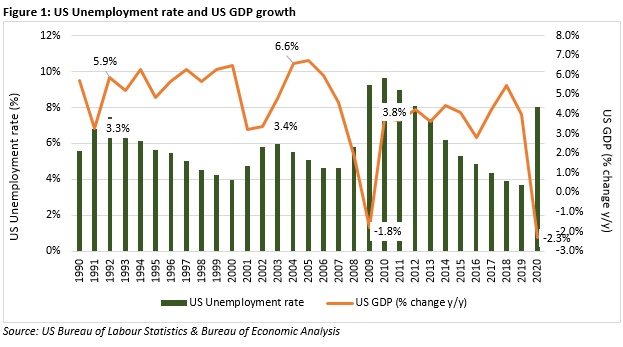

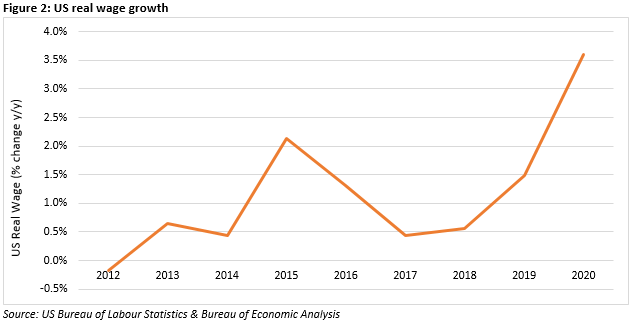

US is the largest importer in the world and constitutes 12.8 per cent of the global imports. For US economy, consumption demand is the largest part (more than 80 per cent) and growth in this component had been slower than it was on average before the global financial crisis (GFC). Post the GFC, US economy had a much slower recovery in demand and resulted in only a gradual reduction in unemployment rate. Figure 1 shows the growth rate in US economy along with the unemployment rate post 1990. The period post the GFC is remarkable as the economic shock was perhaps the largest as compared to some previous crisis (dot-com crisis in early 2000s and economic shock in early 1990s), but the recovery was relatively muted. Unemployment remained more than 6.0 per cent until 2014 and came back to 4.0 per cent only by 2018. This had a tremendous impact on the overall demand in the economy as wage growth in the economy was also slow. Real wage growth remained less than 2.0 per cent for much of the last decade as job creation was slow (Figure 2). Real wage growth generally determines growth in purchasing power of the economy. For most of the economy, wage is the main source of income and therefore expenditure. With a slower real wage growth, a large section of population would have a lower capacity to spend in real terms, their incomes consumed away largely by inflation.

US economy is largely fuelled by consumption demand, while domestic fixed capital formation remained historically very low at 21.0 per cent in 2019. Fixed capital formation or investment in physical assets is an important factor in increasing productivity and bringing efficiency gains for the economy. But this component has moved relatively slow for the US, impacting its growth prospects in the recent years. Particularly lagging was the progress on infrastructure investment where maintenance backlogs remained significant. The 2021 Report Card for America’s Infrastructure prepared by the American Society of Civil Engineers gave a C-ranking to America’s physical infrastructure and calculated the total infrastructure needs in America at about USD 5.94 trillion until 2029.1 The budget may not be adequate to fund the entire requirement, but it will still provide a massive productivity boost.

US economy and global trade

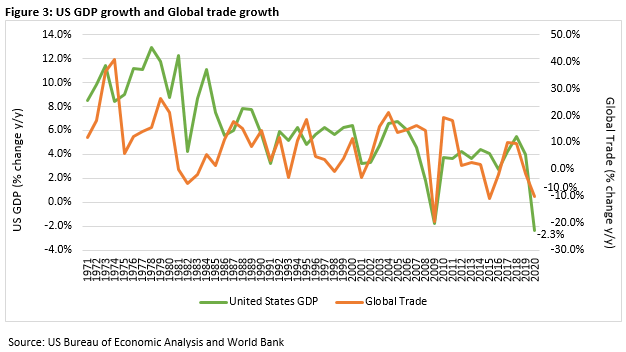

When the US economy grows slower, overall global demand is pulled down. Slower US economic recovery would mean a slower recovery for global trade as well, given the large share of US imports. This is played out in historic data as well, as global trade growth has moved in tandem with US economic growth. Figure 2 shows the two variables stacked against each other. US growth and global trade growth have a strong correlation of 50.9 per cent, suggesting the importance of US economy for global trade.

Infrastructure spending is considered to be the most efficient of all different kinds of fiscal stimulus policies. Fiscal stimulus measures such as unemployment insurance or tax cuts provide a short-term boost in consumption demand. Infrastructure spending on the other hand is usually spread out over multiple years and helps create assets that generate revenue in the future. Apart from the direct stimulus through job creation and generating immediate demand for many related products, there are indirect effects on the economy via increased consumption demand from direct employment gainers, increased savings for businesses through cost reductions, greater access for people to economic activities among others.

Global Infrastructure Hub estimates that on average infrastructure spending has an economic multiplier of 0.8 within 1 year compared with 0.7 for other types of fiscal spending. For a longer-term horizon (2-5 years), it has an even larger multiplier of 1.5 compared to 1.0 for other spending.2 Multiplier effect is generally a feature of the economic impact of public sector spending which reflects direct impact in the year of spending and indirect (ripple) effects in subsequent years. These numbers suggest that an additional USD 550 billion of infrastructure investment could potentially add USD 825 billion to US GDP over the next 10 years. Even if we assume a consistent 10 per cent share of US imports in incremental GDP, global demand will increase by an additional USD 82.5 billion over the next 10 years. A Morgan Stanley report also suggests that US infrastructure demand could potentially lead to a commodity super-cycle for construction materials and provide a major boost to industries in the resource rich economies.3

Gains for textile and clothing industry

Since, global textile and clothing industry was one of the worst hit sectors during the pandemic, it will gain tremendously from a boost in US demand and global trade. US being the second largest importer of apparel, this consumption demand will create the necessary demand for textile and clothing industry in many of its importing nations. Additionally, increasing demand from other countries and rising trade flows would provide a second order stimulus to the textile and clothing industry globally. Another more direct impact would be an increase in demand for geo-textiles and textile materials used in construction. US and China are the two largest markets for geo-textiles, and infrastructure plans of both economies are likely to push this segment further tremendously.

1https://infrastructurereportcard.org/wp-content/uploads/2020/12/National_IRC_2021-report.pdf

2https://www.gihub.org/infrastructure-monitor/insights/fiscal-multiplier-effect-of-

infrastructure-investment/

3https://www.morganstanley.com/ideas/us-infrastructure-investment-supercycle

Comments